For most of 2026, owning XOM and CVX was about as close to a sure thing as the market offered. Then the U.S. Treasury moved quietly in the early hours of June 22, and the trade became a lot more complicated.

Here’s where things stand — and why the next 53 days matter as much as anything else in energy right now.

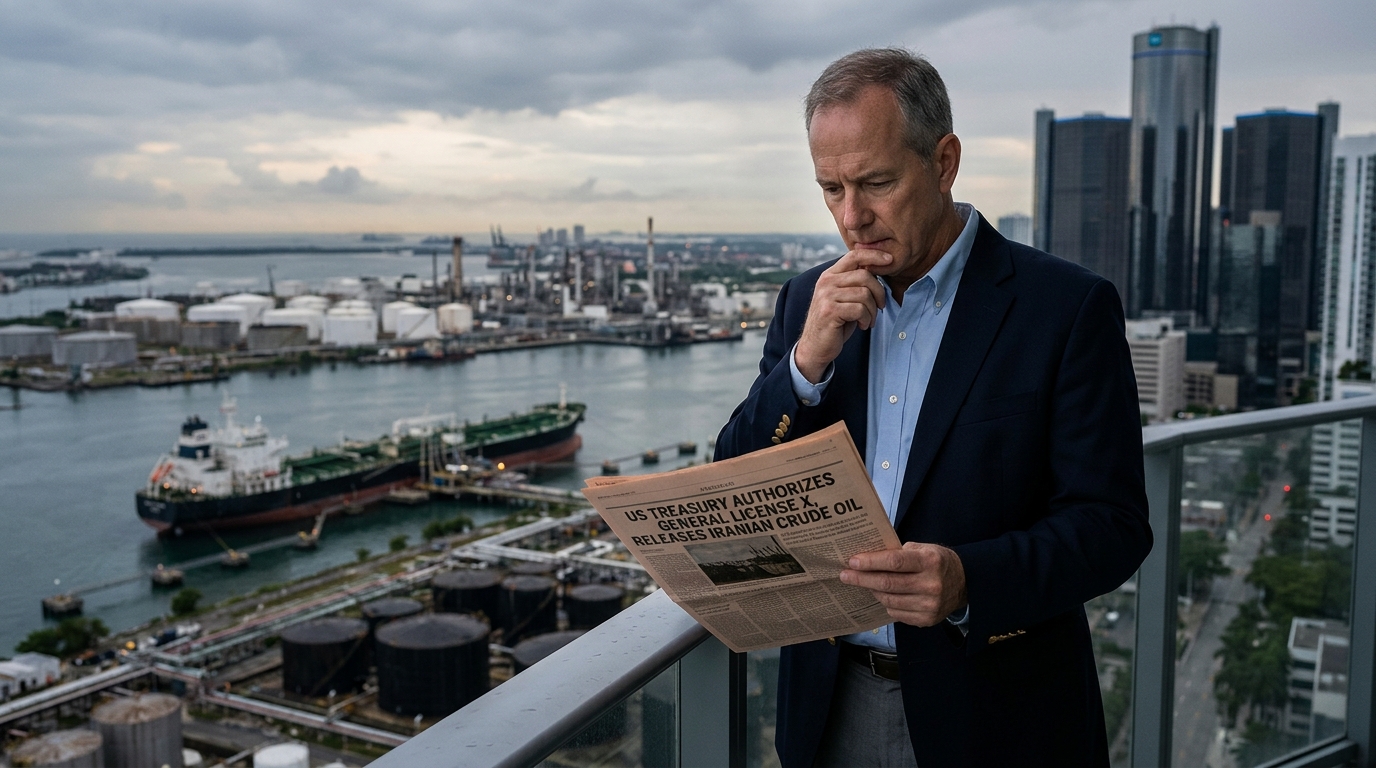

What Happened

The Office of Foreign Assets Control published General License X on June 22. It’s a sweeping 60-day authorization allowing buyers worldwide to purchase, transport, and arrange services for Iranian crude, petroleum products, and petrochemicals, with no volume cap. Buyers can pay Iran directly in U.S. dollar-denominated funds — removing one of the biggest practical barriers to Iranian oil reaching global markets. Brent crude fell more than 3.5% on the day of the announcement, and losses continued through the week.

GL X expires August 21. That date matters more than any earnings call between now and then.

The Setup Heading In

To understand why this stings, you need to understand what 2026 looked like for these two companies through Q1.

Exxon rose 41% in the first quarter. Chevron climbed 36%. Energy led every S&P 500 sector while the broader index fell 4.6%. The Iran war had throttled the Strait of Hormuz — the narrow passage through which roughly a fifth of the world’s oil normally travels — and Brent crude traded up to the mid-$120s per barrel during the spring. Exxon’s Energy Products segment earned $2.8 billion in Q1 excluding identified items and timing effects, up from $856 million a year earlier.

That’s what a supply shock does for an integrated major. And that’s what’s now partially reversing.

Exxon has dropped more than 23% from its $176.41 peak. Chevron is down roughly 20% from its $214.71 high. WTI crude, as of June 25, settled at $69.21 per barrel after falling sharply since late May.

The Business Behind the Headlines

Both companies are integrated supermajors — they span upstream exploration and production, midstream logistics, and downstream refining and chemicals. That diversification is exactly what helps them navigate commodity cycles better than pure-play producers. Exxon’s Permian Basin production and Chevron’s 39-year dividend growth streak provide earnings and income support that’s independent of geopolitical pricing.

Slight tangent, but it’s relevant: Chevron’s acquisition of Hess added direct ownership of the Stabroek partnership in Guyana — long-life, low-breakeven barrels that change the production profile materially over the next decade. That’s a fundamental improvement that has nothing to do with the Iran premium. Same story with Exxon’s Permian scale. Neither company’s underlying business got worse this month.

What changed is the price they’re getting paid per barrel.

The GL X Question

GL X is a 60-day window, not a permanent policy shift. Several dynamics complicate how quickly Iranian barrels actually reach global markets. Many U.S. banks and global insurers remain wary of the license due to ongoing IRGC-related risks, which could slow Iranian crude from reaching market at full scale. Shipping activity through the Strait of Hormuz has picked up since the interim agreement, but there are still reports of disruptions and elevated risk in the region.

If U.S.-Iran talks collapse before August 21 — and negotiations have repeatedly threatened to break down amid ongoing strikes — the war premium could return quickly.

Meanwhile, global oil inventories have been draining fast. ExxonMobil senior vice president Neil Chapman warned that the world is “approaching unheard of inventory levels.” Claims about the exact magnitude of stock draws during the disruption vary by estimate, but the core point holds: rebuilding inventories takes months, not weeks.

Forward Scenarios

Bull: GL X fails to materially increase Iranian supply due to banking and insurance hesitation. Ceasefire negotiations stall. Crude recovers toward $80–$85. XOM and Chevron recoup 10–15% from current levels, supported by Permian and Guyana production economics and dividend income.

Base: Iranian barrels gradually re-enter the market but below what GL X theoretically allows. Crude stabilizes in the $70–$78 range. Both stocks trade sideways through August, underperforming the broader market but protected by buybacks and dividends. GL X either renews or transitions into a formal peace framework.

Bear: GL X works better than expected. Iran pumps aggressively. WTI drifts toward $60. Both stocks give back the remainder of their 2026 premium. Dividend yields widen, attracting income buyers — but capital appreciation stalls until the next supply catalyst.

Technical Overlay

XOM is trading well below its 50-day and 200-day moving averages after the sharp drawdown from the $176 peak. Near-term support sits around $130–$133. Chevron is in a similar position relative to its moving averages, with support in the $155–$158 range. Neither stock has found a clear technical floor yet — the peace premium is still unwinding in real time. The August 21 GL X expiry date is effectively the next hard catalyst for a directional move in either direction.

What Investors Should Watch

- U.S.-Iran Doha talks — U.S. officials have said the two sides are set to meet in Doha this week

- IEA weekly inventory data — global stock draws are the supply-side story that media keeps underweighting

- Shipping volume through Hormuz — actual tanker flows will lag the diplomatic news by weeks

- Permian and Guyana production updates — the fundamental earnings floor for both names

- DOJ probe — Trump said he ordered the DOJ to look into whether oil companies are gouging consumers; any regulatory action would add noise but likely not fundamentally alter the earnings case

Bottom Line

The war premium that powered XOM and CVX to their 2026 highs was real money — but it was borrowed from a geopolitical event, not earned from a business improvement. GL X started giving that premium back. What the market hasn’t fully priced yet is the inventory draw reality: rebuilding depleted inventories takes time, and Iranian crude re-entering a depleted market is very different from Iranian crude re-entering a well-stocked one.

The fundamentals of both businesses — Permian production, Guyana growth, decades of dividend compounding — haven’t changed. Whether the stock prices stabilize depends almost entirely on what happens in Doha this week.

For informational purposes only.